Does Florida Homeowners Insurance Cover Mold? What's Covered

Every Florida summer, the same phone call comes in: someone has found dark staining behind a baseboard or inside an AC closet, and the first question isn't "how bad is it?" — it's "will my insurance pay for this?" It's a fair question, and the honest answer surprises people. The size of the mold problem has almost nothing to do with whether it's covered. What matters is where the water came from.

Florida homeowners insurance generally covers mold only when it results from a sudden, accidental, covered event — a burst supply line, a failed water heater, or wind-driven rain entering through storm damage. Mold that develops gradually, from a slow leak, chronic humidity, or poor ventilation, is excluded by virtually every standard Florida policy as a maintenance issue. Even when mold is covered, most policies cap remediation at a sublimit that's often around $10,000 or less. The cause of the moisture — not the mold itself — decides the claim, which is why documenting that cause early matters more than anything else you'll do.

Why this matters right now

We're in the middle of Florida's rainy season, and peak hurricane activity runs from mid-August through mid-October. This is the stretch when water finds its way into homes — through a roof that's been quietly separating at the flashing, through a window that leaks only in a driving rain, through an AC system working overtime in 90-degree humidity. It's also the stretch when the difference between a covered claim and a denied one gets decided, usually in the first 48 hours, usually before anyone thinks to call an inspector.

As a Florida-licensed mold assessor (MRSA #MRSA5406) and NAERMC Certified Mold Hygienist, I read moisture differently than a general home inspector does — my job on an assessment isn't just to confirm mold exists, it's to establish where the water came from and how long it's been there. That distinction is the whole ballgame with insurance. A homeowner sees mold. An adjuster sees a question about cause. The assessment is what answers it.

The rule that decides every Florida mold claim

Nearly every mold coverage dispute in Florida comes down to a single line: was the water sudden and accidental, or was it gradual?

Insurers cover the first and exclude the second. The logic, from their side, is that a gradual problem gave you the opportunity to find and fix it before it became a mold situation. Whether that's fair in a state where a supply line can weep inside a wall for a year without a visible clue is a separate argument — but it's the rule that governs your policy.

| Usually covered (sudden, accidental) | Usually excluded (gradual, maintenance) |

|---|---|

| A supply line or pipe that bursts without warning | A slow drip under a sink that ran for months |

| A water heater or washing machine that fails and floods | A roof flashing that's been separating for two rainy seasons |

| Wind damages the roof and rain enters during a storm | Chronic indoor humidity above 60% |

| A sudden appliance overflow | A bathroom exhaust fan that hasn't worked in years |

| Fire-related water damage | Blocked AC drain lines and dirty drip pans |

Read that right column again, because it's essentially a list of the most common ways Florida homes actually get mold. That's not an accident — it's why so many mold claims are denied, and why prevention carries more weight here than coverage does.

The sublimit most homeowners never check

Here's the part that catches people even when their claim is approved. Mold coverage is typically capped by a separate sublimit, frequently around $10,000 or less — and that's not the same as your dwelling limit. Typical Florida remediation work commonly runs somewhere in the range of a few thousand dollars for a contained problem, but a large job involving multiple rooms, HVAC contamination, or structural materials can move well past a modest sublimit in a hurry.

Most carriers will sell you an endorsement that raises the mold limit for additional premium. Whether that's worth it depends on your home — its age, its plumbing, its history of water events. What isn't optional is knowing your number. Pull your declarations page and look for the mold sublimit specifically. It takes two minutes, and it's the difference between assuming you're covered and knowing what for.

What we typically see when a claim goes sideways

What we typically see across Palm Beach and Broward is that the denied mold claim is almost never the dramatic one. Nobody loses the fight over a pipe that visibly exploded at 2 a.m. — that one is obvious, documented by the water on the floor, and paid. The claim that gets denied is the AC closet.

Florida air handlers run nearly year-round in high humidity, pulling moisture out of the air by design. When a drain line clogs or a drip pan rusts through, that water doesn't announce itself — it goes into the platform, the drywall behind it, the insulation. By the time there's an odor or a visible stain, the condition is months old, and the carrier reads it exactly as it looks: gradual.

The homeowner did nothing wrong except not look inside a closet they had no reason to open. That's the scenario I'd most want Florida homeowners to understand, because it's the one that's both most common and most preventable.

The homeowner did nothing wrong except not look inside a closet they had no reason to open. That's the scenario I'd most want Florida homeowners to understand, because it's the one that's both most common and most preventable.

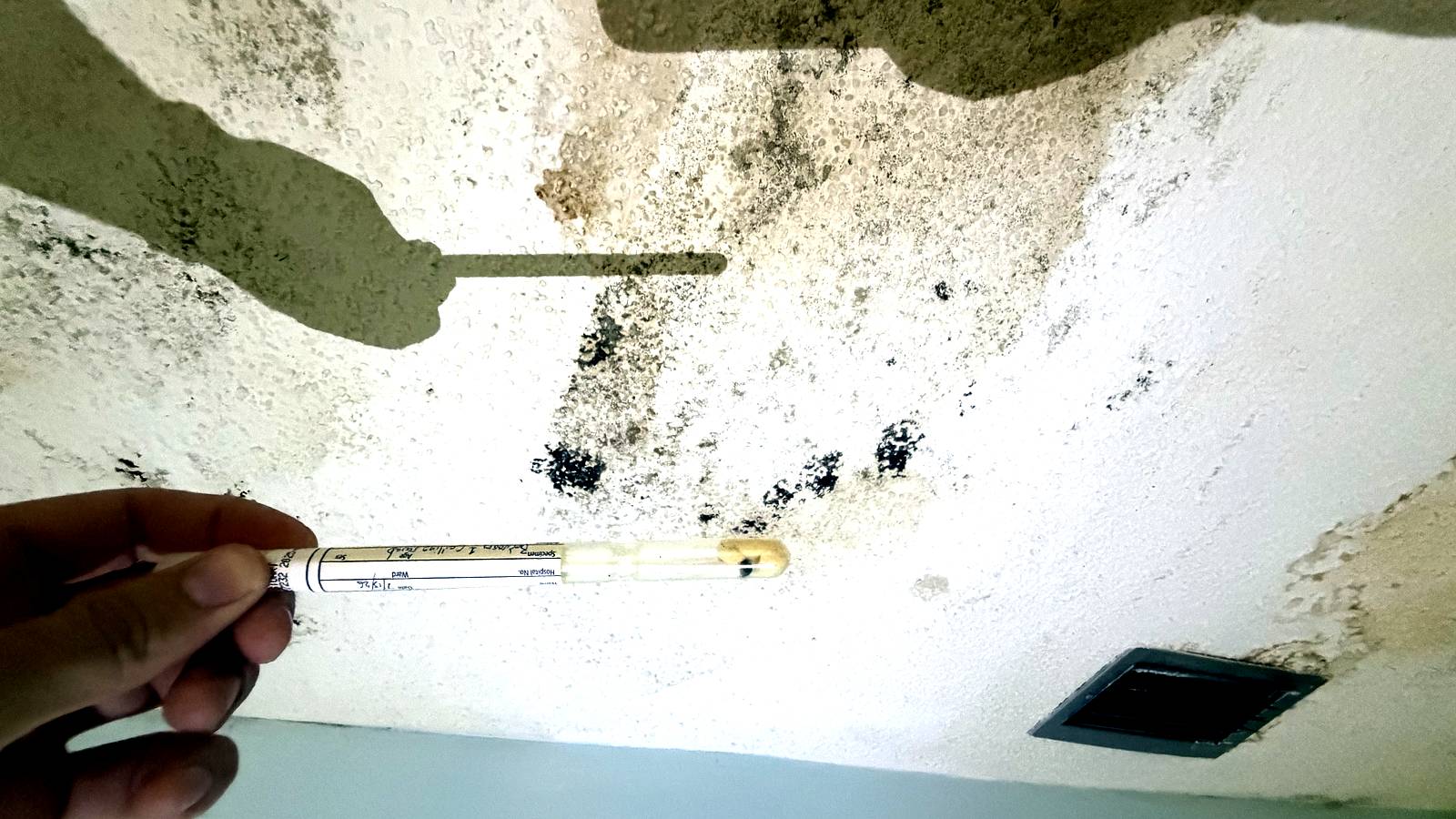

Why documentation — and independence — decide the outcome

If cause determines coverage, then evidence of cause determines your claim. That's what a licensed mold assessment produces: documentation of the moisture source, moisture readings in the affected materials, the extent of what's involved, and lab-backed sampling results. It's the difference between telling an adjuster "there's mold" and showing them what happened.

There's a structural reason to care who writes that report. Florida is one of a small number of states that licenses mold services at all. Under the Florida Mold-Related Services Act, the state issues two separate licenses — MRSA for assessors and MRSR for remediators — and Florida Statute 468.8419 prohibits an assessor from performing or offering remediation on a structure their company assessed within the previous 12 months. Violations escalate from a misdemeanor to a third-degree felony for repeat offenses.

The legislature drew that line for an obvious reason: a company that both diagnoses the problem and gets paid to fix it has a financial incentive to find more of it. Accurate Building Inspections performs mold assessments and does not perform remediation — we have no stake in how large the answer turns out to be. When an adjuster weighs a report, that independence isn't a marketing line. It's the reason the report is credible.

Should you get a mold assessment?

Not every damp spot needs a professional. Here's how I'd decide:

- You've had any water intrusion event — a leak, a storm, an appliance failure — and you plan to file a claim. Get the assessment before anything is dried out, torn out, or repaired. Once the evidence is gone, cause becomes an argument instead of a fact.

- You can smell it but can't find it. A persistent musty odor with no visible source usually means the moisture is behind something. That's a diagnostic problem, not a cleaning problem.

- You're buying a Florida home, especially one that's older, coastal, or has been vacant. Pair it with a full home inspection — mold assessment isn't part of a standard inspection's scope.

- Someone in the home has persistent symptoms that improve when they leave the house. Testing tells you about the building, not about anyone's health — for the health question, see a physician. But if the building is the suspect, air quality testing is how you rule it in or out.

- Visible growth is larger than about 10 square feet — roughly a 3-by-3 patch. The EPA treats that as the rough threshold where professional involvement is warranted rather than DIY cleanup.

If none of those apply and you've got a small patch of surface mildew on bathroom tile from a steamy shower, you probably don't need me. Clean it, run the exhaust fan, and watch it.

Protecting your coverage before you ever need it

Because Florida's climate does most of the damage gradually — the category insurers exclude — prevention is worth more here than coverage is. The EPA's guidance on mold and moisture is refreshingly concrete, and three items carry most of the weight in a Florida home:

- Dry any wet materials within 24 to 48 hours. The EPA is explicit that if wet or damp areas are dried inside that window, in most cases mold won't grow. This single rule prevents more Florida mold than everything else combined.

- Keep indoor humidity below 60%, ideally between 30% and 50%. A hygrometer costs less than lunch. Above 60%, you're not preventing mold, you're scheduling it.

- Keep AC drip pans clean and drain lines clear and flowing. The EPA calls this out by name, and in Florida it's the highest-value maintenance item on the list.

And if you do have a water event: photograph everything before you touch it, stop the source if you safely can, and report it promptly. Don't tear out wet drywall before it's documented — you may be removing the proof that the damage was sudden. If a claim is disputed or denied, that's a conversation for a licensed Florida attorney; my role stops at documenting the building.

Frequently Asked Questions

Does homeowners insurance cover mold in Florida?

Usually only when the mold results from a sudden, accidental, covered event — a burst supply line, an appliance failure, or wind-driven rain entering through storm damage. Mold that develops gradually from a slow leak, high humidity, or poor ventilation is excluded by virtually every standard Florida policy as maintenance-related. The cause of the moisture, not the mold itself, decides the claim.

How much mold coverage does a Florida policy usually include?

Even when mold is covered, most policies cap remediation at a sublimit that's often around $10,000 or less — well under the cost of a large job. Many carriers sell an endorsement that raises the limit for additional premium. Check your declarations page for the mold sublimit specifically; it's separate from your dwelling coverage.

Why do Florida mold claims get denied?

The most common reason is that the insurer classifies the moisture as gradual damage — a slow drip, a long-separated roof flashing, chronic humidity, or a ventilation failure — rather than a sudden event. Delay is the second reason: waiting to report or drying things out before anyone documents the source can make the cause impossible to establish after the fact.

How much does a mold assessment cost in Florida?

A mold assessment with Accurate Building Inspections is $550, and indoor air quality testing is $400. A licensed assessment documents the moisture source, the extent of affected areas, and lab-backed sampling results — the evidence an adjuster needs to evaluate cause.

Can the same company inspect my mold and remove it?

Not in Florida, in most cases. Under Florida Statute 468.8419, a mold assessor may not perform or offer remediation on a structure their company assessed within the previous 12 months. The state issues two separate licenses — MRSA for assessors and MRSR for remediators — specifically to remove the incentive to find more mold than is actually there.

What should I do the moment I find water damage?

Photograph everything before you disturb it, stop the water source if you safely can, and report it to your carrier promptly. The EPA advises drying wet materials within 24 to 48 hours, because in most cases mold won't grow if the area is dried inside that window — so act fast, but document first.

This article kicks off our Florida Mold & Indoor Air Quality series. Upcoming articles will cover:

- What a Florida mold assessment actually involves — and why your assessor shouldn't be your remediator (coming soon)

- Mold after a storm: the 24–48 hour window that decides everything (coming soon)

- Why your AC is the #1 mold source in Florida homes (coming soon)

If you're also navigating Florida's insurance market on the coverage side, our Florida Insurance Inspections series covers the inspections that affect your policy directly:

- Florida's new wind mitigation form and how much you can save

- What a Florida 4-point inspection covers — and what fails one

You can also meet the inspectors behind these reports.

Schedule Your Mold Assessment

If you've had a water event, you can smell something you can't find, or you're buying a home you're unsure about, an independent assessment answers the question that actually decides your claim: where did the water come from, and how long has it been there?

Accurate Building Inspections performs licensed mold assessments and indoor air quality testing across South Florida and Central Florida, including Delray Beach, Fort Lauderdale, and Boca Raton. A mold assessment is $550 and indoor air quality testing is $400, with lab-backed, photo-documented reports. We assess — we don't remediate — so the findings are independent of who profits from the fix.

Schedule online or call (786) 863-4866.

Sources: U.S. Environmental Protection Agency, A Brief Guide to Mold, Moisture and Your Home and Mold Course Chapter 9; Florida Statute 468.8419 (Mold-Related Services); Florida DBPR; Centers for Disease Control and Prevention — Mold.

Frequently Asked Questions

Schedule your inspection

Ready to put this guidance to work? Our licensed Florida inspectors are here to help.